Learning Objectives

- Inform your decision to split your Common Good Plan savings between a TFSA account and/or an RRSP account

- Learn why modest-income individuals may want to allocate retirement savings into a TFSA

- Learn why middle- to higher-income individuals may want to allocate retirement savings into both TFSAs and RRSPs

Key Insights

- The Common Good Plan includes both an RRSP and a TFSA

- Modest-income individuals will want to save for retirement using a TFSA, not an RRSP account

- Most middle- to higher-income individuals will need both TFSAs and RRSPs: While an early-career individual might begin saving with only one of these two account types, most may want to consider contributing to both types of accounts in order to successfully meet long-term retirement savings goals. For those who earn $50,000 or less, the default option is to max out your TFSA account on a monthly basis before contributing to an RRSP

- Both RRSPs and TFSAs provide tax-advantaged savings opportunities, but there are important differences between them, such as how they are taxed and how contribution limits are set

- As you’re accumulating retirement savings in your TFSA and RRSP, you’ll need to ensure you don’t exceed the contribution limits for these accounts — your annual Notice of Assessment and/or an online account with the Canada Revenue Agency can help you keep track of what your limits are

TFSA vs. RRSP?

If you’re thinking about saving for retirement, you’re probably familiar with these two tax-advantaged savings accounts: the Registered Retirement Savings Plan (RRSP), and the Tax-Free Savings Account (TFSA). The Common Good Plan includes both account types.

Both accounts were established to help Canadians save, and both have limits to how much you can contribute each year. But there are important differences between the two.

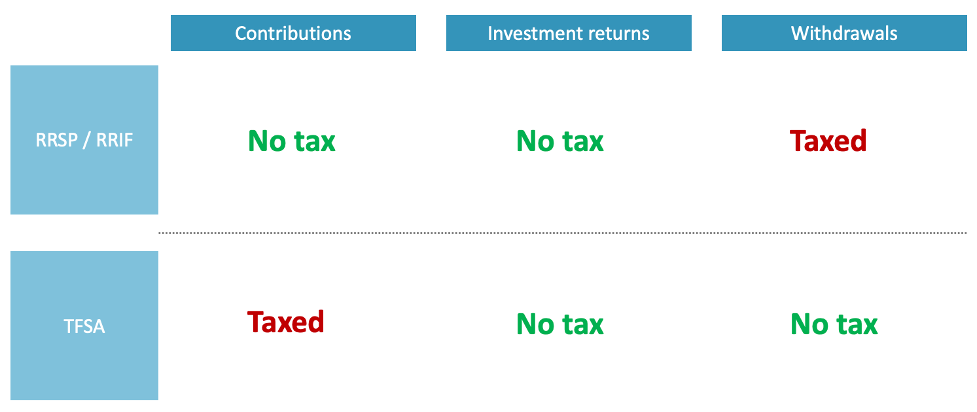

When you add funds to a TFSA, you are making contributions from income you’ve already paid tax on. Since you’ve already paid tax on any funds that you put into your TFSA, you cannot deduct TFSA contributions from current income. Your contributions grow tax-free while they’re in the TFSA account, and you aren’t taxed on any withdrawals. For 2024, you can save up to $7,000 in your TFSA, regardless of your income. This contribution room grows each year if you don’t use it. The total potential contribution room since the TFSA was created in 2009 is $95,000.[1]

In contrast, when you add funds to save through an RRSP account, you are making contributions from pre-tax income (meaning the amount of your contribution is deducted from your current income before it is taxed). Your RRSP contributions grow tax-free while they’re in the plan but are taxed on withdrawals for retirement income.

TFSA vs. RRSP: Tax Treatment

There are some additional considerations that differ depending on income level and individual circumstances.

Modest-income individuals – TFSAs are usually best

If you earn less than $50,000 per year and do not have a workplace pension and/or a large RRSP account, you are likely better off saving using a TFSA.

One reason for this is that modest-income individuals may qualify for the Guaranteed Income Supplement (GIS). The GIS is a program for seniors at and above age 65 with modest incomes. If you qualify for maximum GIS benefits, you would get ~$11,000 / year.[2] About one third of Canadian seniors qualify for GIS.

If you qualify for GIS, you will likely not want to save using RRSPs. This is because doing so will mean getting less GIS benefits. RRSPs must be converted to a RRIF by Dec 31 of the year you turn age 71. When an RRSP becomes a RRIF, you must withdraw a minimum amount of money each year from your RRIF. For every dollar you withdraw from your RRIF after age 65, your GIS is reduced by at least 50 cents.

There is no impact on your GIS if you save in and withdraw from TFSAs.

Another reason why TFSAs tend to work better when you have a modest income is that you are in a lower tax bracket. That means that the RRSP deduction will not be worth as much to you as someone who is in a higher tax bracket.

| Saving through… | ||

| TFSAs | RRSPs | |

| Impact on your GIS benefits | No impact | Reduces GIS benefits by at least 50 cents on the dollar per RRSP dollar withdrawn |

If you have already been saving in an RRSP and qualify for GIS, you may want to consider converting your RRSP into a TFSA.[3]

The Government of Canada provides additional information explaining the impact of savings in non-TFSA accounts on federal income-tested benefits and credits including GIS.

Middle- to higher-income individuals – Use RRSPs and TFSAs to save

If you earn over $50,000 per year, RRSPs become more attractive as retirement savings vehicles. First, middle- and higher-income earners are unlikely to qualify for GIS, so using the TFSA to avoid a GIS “clawback” is not likely to be relevant. Second, middle- and higher-income earners are in a higher tax bracket, and therefore receive a larger benefit from the RRSP deduction. They are also more likely to be in a lower tax bracket when they retire than whey they are working, meaning they can often save on taxes by deferring those taxes until later, which is what happens through an RRSP.

Even if you are using RRSPs as your primary retirement savings vehicle, there are still reasons to consider supplementing your RRSP savings with savings through a TFSA. Some people, especially higher-income earners, will need to save more than the RRSP limits allow. For these people, saving through a TFSA is a good option because investment earnings are not taxed.

TFSAs are also useful because, unlike RRIF withdrawals, TFSA withdrawals do not affect your Old Age Security payments. For Canadians whose net income in retirement is about $80,000 or higher, their OAS payments are reduced by 15 cents for every dollar of taxable income. RRIF income counts towards this taxable income figure. TFSA income does not.

Another factor to consider is the ultimate use of funds saved in either a TFSA or RRSP. If you withdraw from your TFSA, your TFSA contribution room is restored (with exceptions) at the beginning of the following calendar year.[4] If you withdraw from your RRSP, your contribution room will not be restored. TFSAs may be helpful in the case of emergency situations when you might need some flexibility for temporary changes in financial needs.

The Common Good Plan includes both TFSAs and RRSPs

With the Common Good Plan, you can choose how you want to split your savings between your TFSA and RRSP accounts, but the plan offers a suggestion based on your annual income.

For those who earn $50,000 or less, the default option is for members to max out their TFSA on a monthly basis before contributing to an RRSP. This default is based on what is tax-efficient for these members, and considers a lifecycle approach, which prioritizes saving in a TFSA earlier on, when earnings may be lower, and then later on prioritizes adding savings in an RRSP as earnings — and thus tax deductions from RRSP contributions — increase over time.

If obtaining a tax deduction on current earnings is your priority, you can direct your savings to first go into an RRSP and contribute to a TFSA only once you have reached the maximum of your RRSP contribution room. If you contribute into both RRSP and TFSA, you would be able to get the corresponding tax benefits from each.

Know Your Limits: Managing RRSP and TFSA contribution room over time

The amounts that you can contribute to a TFSA and an RRSP are set by Income Tax Act rules. This means that you need to ensure that you don’t exceed your available “contribution room” in all your TFSA and RRSP accounts. Overcontributions are subject to penalties. As a member of the Common Good Plan, it is your responsibility to make sure you don’t exceed your contribution limits for each account type.

Your contribution limit is unique to you and takes into account new contribution room that you generated each year, as well as any past unused contribution room amounts from previous years. One way to track and manage your contribution room over time is through the My Account service provided by the Canada Revenue Agency, which is “a secure online portal that lets you view your personal income tax and benefit information and manage your tax affairs online.”[5]

RRSPs and TFSAs: A comparison

| RRSP | TFSA | |

| History | • Introduced in 1957 to provide a tax-deferred retirement savings account for Canadians without employer-sponsored pension plans | • Introduced in the 2008 federal budget as a “flexible savings vehicle” for Canadians • Came into effect on January 1, 2009 |

| Impact on Guaranteed Income Supplement | • Reduces GIS benefits by at least 50 cents on the dollar per RRSP dollar withdrawn | • No impact |

| Tax implications | ||

| Contributions | • Deducted from your taxable income | • Made from after-tax income (no tax deduction for contributions) |

| Investment earnings (while your savings are in the plan) | • Never taxed | • Never taxed |

| Withdrawals | • Taxed as income | • Never taxed |

| Maximum yearly contribution | • Based on a percentage of your “earned income” for the year, to a maximum set by Income Tax Act rules • In 2024, the maximum you can contribute to an RRSP is 18% of your earned income to a limit of $31,560 (minus pension accruals if you have a pension plan) • You can make additional contributions if you have not maximized contributions in previous years | • Not dependent on level of income • Available to all Canadians age 18 and over • 2024 contribution limit is $7,000 • You can make additional contributions if you have not maximized contributions in previous years |

| Maximum age allowed for making contributions | • End of the year when you turn age 71, TFSA | • None |

| Where to find your contribution room | • The My Account service provided by the Canada Revenue Agency (CRA) • Your yearly Notice of Assessment, which you receive after your tax return has been reviewed and assessed by the CRA | • The My Account service provided by the Canada Revenue Agency |

The Government of Canada provides additional information about RRSPs and TFSAs.

References